Equity markets are on a tear – what’s an investor to do? My non-market friends tell me I must be making a killing while everything I look at (ex fixed income related) seems extended and overbought. Go West young man is outdated, especially in today’s world; Go East is flavor du jour. Go North implies cold, dark winter. I say Go South investor; go south, south to the laggards, south to the lands leveraged to what the IMF is calling the broadest and best economic recovery in years if not decades.

There are few things better than a leveraged laggard and yet that is just what is on offer across the southern parts of all three of the Tri Polar World’s (TPW) main regions: Europe, Asia and the Americas. Europe’s Southern Tier, the Southeast Asian nations of Asia and South America within the Americas are all worth a look. Since the March 2009 low each has been a major laggard not only versus the US, the clear front-runner, but also within their respective regions. Most are extended on a short term basis but should be areas of focus on any pullback.

As Chart 1 shows the US equity market has been a dramatic outperformer since 2009, significantly outperforming the other regions. Yet as has been argued here for some time (2017 Global Investment Outlook: America First? December, 2016) last year was the first year since the crisis where the non-US markets outperformed the US in USD terms. As Chart 2 shows these periods of outperformance tend to last for some time, in fact an average of five years plus. We are at the beginning of a period of non-US outperformance; a period that should last for several years.

The non-US markets are leveraged laggards in that they are the biggest beneficiaries of a sustained global growth recovery. In other words the longer the economic recovery lasts the better for these markets. In many cases their domestic economies have more slack than the late cycle US economy which is in its 9th year of expansion versus roughly a third of that for Europe and even less for Latin America. Thus more room for growth, more room for profit expansion, more room for offshore investment, and more political breathing space. Past periods of non-US outperformance support this thesis with the Latin American markets in particular demonstrating leadership.

These markets are also beneficiaries of another trend that may be in its early stages – that of USD weakness. Solid growth combined with a weak dollar presents a very favorable environment for these markets. Our Global Risk Nexus (GRN) Monitoring System suggests that the US is late cycle in all four of its segments: economics, politics, policy and markets. A late cycle economy; political dysfunction and scandal with the Mueller investigation looming like a thunderhead. Oh and did I mention the upcoming mid term elections?

Policy wise the Fed leads the global Central Bank tightening process while ill-judged fiscal policy expands the twin US trade & budget deficits. US equity markets are extended, expensive, overbought and over owned. Table 1 shows how the weak dollar has saddled non-USD investors with fixed income losses, helping to explain why Chinese and Japanese UST buyers may become scarce on the ground. Is it any wonder that European sovereign debt offerings by Italy, Spain and others are being met with massive demand? Did you know that the Greek 2 year bond now yields less than the UST 2 yr.?

Given the equity run since 2009 and the European worries since 2012 its no surprise that investors are very overweight US financial assets. This is starting to unwind as investors of all stripes begin rebalancing back into the Euro, the Yen and even the RMB. The weak dollar set up is very similar to the 2004 period when the Fed was raising rates while the rest of the world grew and the dollar fell. Dollar weakness is a flow story not a relative yield story; it’s a story of relative growth rates and asset allocation and it is arguably early in the process. With the USD breaking down technically, one can see another 10% or so downside, a prospect seemingly welcomed by the US Treasury.

One of the main benefits of the Tri Polar World framework is it allows one to look at the world differently, in this case, through regional eyes. Davos observers have noted the clearest theme emanating from that confab, a theme encapsulated in a quote from Indian PM Modi’s Davos speech: “Everyone talks about an interconnected world but we have to accept the fact that globalization is slowly losing its luster. The solution to this worrisome situation is not isolation. The solution is in understanding and accepting change”.

The Tri Polar World framework does just that. It understands and agrees that globalization has lost its luster, it accepts and provides a framework to incorporate change and given that we are investors it provides a solution which allows investors to make sense of, participate in and benefit from these changes.

Lets utilize the TPW framework to examine each main region in turn and identify the leveraged laggards.

RESURGENT EUROPE

We have been keen on Europe for well over a year arguing that Brexit & Trump would be bullish, not bearish, for European integration. Now that this has become somewhat common wisdom more is required. That means looking at Europe’s Southern Tier as a region ripe for outperformance. As Chart 3 illustrates, the region has woefully underperformed Europe itself since the crisis lows. Among the three, Greece remains deep in negative territory while Portugal is just turning positive; Spain is well in positive return territory but still lagging far behind Europe as a whole. Taken together they are barely positive almost nine years later.

Europe itself is growing faster than it has in over a decade with January PMIs the best in 13 years. The Franco – German motor of European integration is starting to rev up and barring a dramatic reversal in German politics the M&M twins, Merkel and Macron, are ready to lead deeper integration. Europe is finally emerging from its crisis period and recognizing the need to compete against the US and Asia, something French PM Macron understands perhaps better than any Western politician.

European economics are in great shape with a large current account surplus suggesting Euro strength will not hurt exports. That same Euro strength will likely lead the ECB to go slower than it might otherwise go in raising rates as the FX effect dampens inflationary impulses. Economics, politics, policy are all in very good shape.

European equity markets are overbought in the immediate term but otherwise are in good shape with decent earnings growth, reasonable valuation and plenty of room to grow in offshore portfolios. Europe is effectively a value play given its low tech weight. In fact, broad EU equity has performed almost in line with Global value (GVAL) over the past four years. An incipient shift from Growth to Value could provide further support to the EU equity story. Banks (EUFN) long a favored sector, trade at a significant P/BV discount to US banks, have broken out and offer a hedge against inflation & Euro strength, while benefitting from higher rates and a better economy. European small caps (IEUS) also fit a similar bill in terms of the currency issue.

A Europe early in its recovery suggests that the real opportunity lies within the regional laggards, thus the appeal of the Southern Tier. Greece should exit its bailout program in 2018, has already accessed the FI capital markets and offers dramatic upside on a medium term view (near term GREK is overbought). Portugal (PGAL) is making headway on its recovery and likewise offers significant upside to a long lasting European economic revival. Spain (EWP) was just returned to investment grade by Fitch leading its most recent bond offering to be massively oversubscribed. Investors have ridden through the Catalan independence issue and come out the other side. The three markets combined represent only 6% of Europe’s equity market suggesting a significant overweight within a European regional portfolio on a 1-3 year basis.

PROACTIVE ASIA

Japan and China have been the two favored markets in this region over the past year plus and remain well thought of. Japan (EWJ) is exiting inflation, has a very cheap currency (fair value is considered in the low 90s vs. 109 to the USD today), is lifting the lid of the stock market’s long term “iron coffin”, has attractive valuation, good earnings growth and a stable political structure with PM Abe just returned for another term. Small caps (SCJ) are attractive as well here as an offset to Yen strength and a play on Japan’s industrial base.

China (FXI, MCHI, OBOR, DSUM) has been declared about to collapse almost too many times to count since the mid 1990s and yet its leading the way to Asian integration thru its Belt and Road Initiative (BRI), the Asian Infrastructure Investment Bank and numerous other fronts. As in Japan, President Xi has just been returned for another term focused on SOE reform (finally well underway), cleaning up pollution (likewise) & slowly deflating the debt bubble.

But there is more to do in Asia. ASEAN, the Association of South East Asian Nations, is the fourth big player in Asia, joining Japan, China and India. ASEAN is where growth is really taking off and thanks to the wonderful world of ETFs there is a way to invest, namely ASEA. As Chart 4 shows, ASEA has been a dramatic regional underperformer over the past several years. ASEA provides exposure to Malaysia, Indonesia, Thailand, and the Philippines etc. all in one vehicle. As China moves up the value added curve with its focus on China 2025, ASEAN is the big winner, gaining investment, building its own consumer base while selling more to China’s rapidly growing domestic market – it is leveraged to the biggest trends in Asia. As with the European Southern Tier strategy, ASEAN represents roughly 9% of the Asian Pacific equity market; one should consider a significant overweight on a 1-3 yr. basis.

INACTIVE AMERICAS

It’s almost sad to watch the US struggle, at home, abroad, on domestic economic policy and foreign policy. America First is well and truly turning into America Alone, alone and asleep at the switch as the rest of the world moves faster and further. Michael Moritz of Sequoia Capital captured this perfectly in a recent FT op ed comparing Silicon Valley to China’s tech ecosystem (Silicon Valley would be wise to follow China’s lead).

Instead of using the NAFTA negotiations to deepen integration in the Americas & thus improve its competitive position versus Asia and Europe, America threatens to tear up NAFTA. Such a move would top President Trump’s decision to pull out of the Trans Pacific Partnership (TPP), itself going ahead without the US. That last phrase is something those of us in the US are going to have to get used to I am afraid. As an investor, one can only be thankful that the world is our oyster. First step is recognition, second step is action.

Investment opportunity in the Americas extends well beyond the US; there are all those markets South of the Rio Grande: Mexico, Brazil, Peru, Chile, Argentina etc. And again, in the wonderful world of global investing circa 2018 there is an ETF (ILF) that provides exposure to the whole region. As Chart 5 shows Latin Americas has been a massive underperformer relative to the US since 2012. But here too we may be on the cusp of a turn with LA performing in line with the US last year, even with the NAFTA threats, Brazil’s political woes, Chile’s elections etc.

It’s hard to argue that Latin America is in great shape in any of its four segments: yet its economies are improving and are leveraged to the global economic recovery through commodity demand and US demand. In past periods of non-US outperformance, LA markets have been top performers in part because of that commodity exposure. LA is early in its economy recovery with Brazil just emerging from recession; there is plenty of room to grow. On the political front there are elections in both Mexico and Brazil this year and coupled with the policy mix of NAFTA it is clear that Mexico at least will face some challenges.

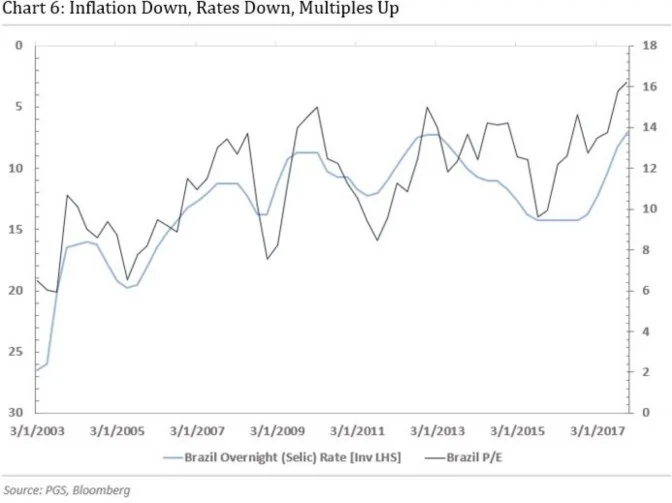

Brazil is the more interesting case (EWZ, EWZS). Following a deep recession, inflation is at almost record lows, bringing down interest rates which in turn pushes money into both domestic & foreign equity. Brazil has long been seen as a very cheap equity market due mainly to sky high real rates. As Chart 6 shows, that dynamic is in flux. As real rates shrink, the economy grows, the currency trades towards fair value, earnings pop and PE multiples expand. Unlike much of the rest of the world which is searching for inflation, Brazil welcomes lowflation. It’s a compelling story.

ASSET CLASS LAGGARDS

Before closing it’s worth pointing out that there are laggards on the asset class front as well. It is true that both equity and fixed income have done well in the past few years. A global 60-40-equity/debt portfolio was up roughly 15% last year and up roughly 9% per annum over the past three years. Arguably this benchmark will face tougher sledding in the years ahead as the sustained global economic recovery allows Central Banks to slowly raise rates, which in turn implies the 40% fixed income portion will struggle.

As Chart 7 points out the gap between stocks, bonds and commodities has also been vast over the past 5 years. In our 2018 Outlook (2018 Outlook: The Global Struggle Between Economics, Politics, Policy & Markets December, 2017) we highlighted the appeal of the commodity space, arguing that it had been thru a period of significant underperformance and as a result funds were closing, sentiment was horrible and the stage was set for relative outperformance, especially given growing inflation concerns. Opportunities exist in broad commodity exposure (DBC), nat gas (UNG) given China’s growing demand, and precious metals (GLD) among others. The ETF ecosystem has really fleshed out the commodity front; something that is likely to prove very useful in the years ahead.

Hopefully the above provides some food for thought and the charts/table are useful. More exciting advances to come in the months ahead. Stay focused my friends.