The first quarter of the year had something for everyone; from January’s melt up to March’s meltdown the one constant was the return of volatility. A few weeks into Q2 and that volatility remains with us as financial markets gyrate to a new geo political tune on a daily basis. For all the angst the first quarter offered muted returns as global equities slipped slightly, bonds rallied a bit while commodities came off the floor to lead the multi asset pack.

In thinking about what Q2 might bring, it struck me that one can think of the outlook as akin to a three on three schoolyard basketball game. On one side we have the 3 Ts: Trump, Tech and Tariffs and on the other we have the 3 Es: Economic growth, corporate Earnings and investor Enthusiasm. If the 3 Ts win it is likely that they will snatch defeat from the jaws of victory as the synchronized global recovery & robust financial markets give way to self-inflicted uncertainty.

To handicap the game’s outcome it makes sense to analyze the player matchups using both our Tri Polar World (TPW) framework and Global Risk Nexus (GRN) Scoring System to analyze the interplay between economics, politics, policy and markets. The 3 Ts in particular seem to validate the TPW theme of regional integration in Asia, Europe and the Americas. Once we run through the matchups we can isolate some plays or investment positions that we think might help win the performance game.

THE 3Ts: TRUMP, TECH AND TARIFFS

President Trump has freed himself from his handlers and is effectively running US domestic and foreign policy himself. Investors now have to come to grips with policy by tweet, policy that is capable of being reversed within a day, a week, a month or not at all. The President is effectively at war on three fronts: politically via the Mueller investigation, economically via the trade conflict with China and militarily via a potential conflict with N. Korea. This degree of conflict coupled with Pres. Trump’s very public policy process generates uncertainty, which markets hate. Thus, this type of policy making represents a valuation ceiling for global equities in general and US equities in particular.

This might not matter so much if the tech sector, the global equity market’s leadership sector, was firing on all cylinders. However, as recent weeks have shown, this is no longer the case. Being hauled before Congress (in the case of Facebook) and having to justify a business model that no one seemed to care about before the 2016 US Presidential elections suggests that the political class is now aware that the tech industry has amassed both profit making and political power. This combination is unlikely to go unchallenged in the months and years ahead. Given that tech represents 25% of the S&P index (and 27% of the broad Emerging Market equity index) what happens to tech matters, a lot.

The Cambridge Analytica data breach seems to have been the straw that broke the camel’s back, calling into question the seemingly inexorable rise of tech’s social media segment in particular. The tech ecosystem now resides squarely in the geo political space & not just for privacy reasons as the US and China square off on AI. Europe sits between the two, seemingly content to play regulator in chief as exemplified by its upcoming GDPR (General Data Protection Regulation) policy. Governments around the globe seek more tax revenue from the big tech piggy bank while in China social media censoring reaches new levels. Competition is also increasing between the various tech segments suggesting a trifecta of tech concerns: privacy regulation, taxation and anti trust. Bottom line: increasing political confrontation around the globe suggests the tech sector’s unbridled pursuit of profits has reached its end game.

Thus the question of equity market leadership. We are on record as believing that global equity markets are early in the process of shifting leadership from the US to the non-US markets. Might we also be early in the transition away from tech led growth to sectors like Financials, Industrials and Energy perhaps? Financials would seem to have the best claim for new leadership: representing 14% of the US market and 18% of ACWI, financials offer good earnings growth, attractive valuation and protection from currency fluctuation while benefiting from rising rates and a solid economy which supports both loan growth and bad debt reduction. Yet the investor response to strong Q1 US bank earnings has been decidedly disappointing to a bank bull such as myself (on both sides of the Atlantic). Sell offs on good news is rarely a positive signpost. Equity sector leadership remains an open question.

What about trade wars and tariff threats? So far it’s more threat than fight but financial markets, equities especially, are forward discounting mechanisms and so investors have been trying to price in what a trade war would look like. Most working estimates suggests the current state of play if implemented would shave off 20-30 bps of economic growth from the major actors suggesting the equity market reaction has been perhaps a bit excessive. Bond market failure to follow the equity market lead and rally in face of growth damaging tariff threats supports this sense.

No one really knows what the White House’s ultimate aim is, whether this is all for show and is simply a negotiating tactic or if there a real intent to punish China and limit its (rising) geo economic influence. Arguments can be made on both sides with the relatively smooth wrap up of the US – Korea trade pact & the US desire to declare victory in the NAFTA redo suggesting the former. However, on the latter side is the long history of Pres. Trump’s China trade views. For its part, China’s reaction has been quite measured, responding in kind to US moves on a parallel basis rather than leading or accelerating the process. Clearly China enjoys having the moral high ground as folks try to wrap their head around a US message that damns the WTO and claims everyone is taking advantage of it in a trade system it effectively set up.

Bottom line one should invest as if tariffs of some degree will take effect. Pres. Xi and Pres. Trump are mano a mano here and neither can really afford to blink. China is not going to give up on its Made in China 2025 program given its economic imperative to move up the value add ladder and offset its rising cost structure. The US would seem to have form in terms of its complaints about the challenges of doing business in China as well as the technology transfer issues. China may well be happy to lose a few trade battles that in actuality support its economic opening and rebalancing process. Early signs (auto/financial market opening) suggest this is the case. Worry about Yuan devaluation seems overdone especially given China’s petro Yuan iniatative. The good news is that room for compromise exists and both leaders have the wherewithal to make decisions should they wish to do so.

SNATCHING DEFEAT FROM THE JAWS OF VICTORY

A feeling of frustration is understandable given how smoothly things seemed to be going just a few short months ago: the best synchronized global economic recovery in a decade or more, the Middle East's principal conflict between Sunni Saudi Arabia and Shia Iran potentially defused as the Iran nuclear deal took hold, revitalized global trade flows after a long post 2008 lull, a gentle unwind of Central Bank liquidity largesse and financial markets that while heated did not seem excessive. Victory over the post GFC slow growth & deflation fears appeared at hand while the absence of bottlenecks and excesses provided hope for a sustained expansion. Was it all just a pipe dream? Thus to the 3 Es.

The solid global economic growth recovery of 2016 to date appears to be cresting with 2/3s of countries running above potential (especially in Europe and Japan). Economic surprise indices have fallen sharply and in the case of Europe to five year lows (suggesting a possible rebound?). Retail sales on both sides of the Atlantic have disappointed while manufacturing PMIs appear to be rolling over across the globe, albeit from levels that still suggest expansion. In the US at least, weak demand would seem to be the culprit as soft real hourly earnings growth coupled with high debt levels and low savings rates impede consumption.

Europe’s apparent slowdown is harder to figure out; weather and political uncertainty given election issues in Germany, Italy and Spain have been named as culprits together with the ebbing of ECB QE and Euro strength. Yet, Europe’s current account surplus (and Germany’s) remains quite high, suggesting that the Euro is not overly strong. Such a surplus also suggests an opportunity for Europe to utilize fiscal stimulus to boost domestic demand and dovetail with the US fiscal stimulus to generate a real boost for the global economy. Recent above inflation pay deals for Germany’s public sector unions is a good first step.

Resurgent Europe, as it is known in the Tri Polar World, has a real opportunity to help itself and the global economy while reducing the risk of being picked on for its large surplus. Time will tell but the early 2018 read on the Macron & Merkel tandem is less robust than one would have hoped. In addition to fiscal stimulus, there is a real opportunity to marry Macron’s vision of Europe with Merkel and Germany’s pragmatism especially around banking reform and the transition of the European Stability Mechanism (ESM) to a European monetary fund. The M&M twins need to grasp the nettle.

Earnings have been quite robust as noted in earlier writings ( 2018 Outlook: The Global Struggle Between Economic, Politics, Policy & Markets December 2017) and provide good support to current global equity levels. As Chart One indicates the combination of a roughly 10% decline in price coupled with a 7% or so increase in forecast earnings has brought the forward PE of the S&P down to 16.5 from roughly 20 a few months ago, positioning it as cheap as it has been in the past three years.

Chart 1: SPX Improving Valuation

While tax-augmented earnings growth appears most robust in the US at roughly 18% for 2018, EPS growth (USD) in Europe and Japan at 12% and 10% are also robust. Furthermore, Chart 2 suggests that Europe’s relative valuation vs. the US have not been this compelling since the mid 1990s, which is saying something. Within European equity, the financial sector, a PGS preferred sector, trades at roughly one times book value and under 11x forward earnings. This represents a significant discount to the US banks as well as to Europe’s valuation at roughly 13.5x.

Chart 2: EU Cheapest vs. US Since the Mid-1990’s

The set up heading into Q1 earnings season was quite attractive with markets having been beaten down by the 3Ts and investor enthusiasm, white hot back in January, having cooled significantly as Chart 3 suggests. This of course is good news as depressed sentiment provides room for things to turn around and inspire buyers to step in. While retail investor sentiment has clearly cooled evidence suggests hedge funds and the CTA community have also sharply reduced their long equity positions.

Chart 3: Bearish Sentiment Is Bullish

Much depends both on where the economic recovery goes from here together with the earnings path through the rest of the year and into 2019. Time is passing and by the middle of Q3 investors will be starting to turn their sights to US midterm elections & what appears to be a big Blue (Democrat) wave as well as the 2019 outlook and what it might offer. The shape of the global economic recovery will have a big role to play in that picture and here we come back full circle.

Tariff threats could lead to a rapid descent of C suite confidence thus leading to a reduced cap ex cycle that many have been counting on to increase productivity and hence sustain the global recovery. The absence of such would imply a global expansion and an aging US expansion in particular that is much closer to its end date than would otherwise be the case. The record number of times tariffs have been mentioned in Q1 earnings calls suggests this is a real threat to continued confidence and investment.

There are two hints of a silver lining however; first that such an ebbing of C suite confidence could lead to executives falling back on their old standby of stock buybacks which would support equity market prices and second, tariff threats and political uncertainty would likely lead the world’s Central Banks to adopt a go slow pace in withdrawing monetary accommodation which remains robust as Chart 4 indicates. In fact in recent speeches both Fed Chair Jay Powell and ECB head Mario Draghi used the term “patient” to describe how they expect their banks to act in the current uncertain environment. That is good news for risk assets

Chart 4: Global Liquidity Remains Robust

PORTFOLIO STRATEGY AND ASSET ALLOCATION

The pick up game between the Ts and Es suggests continued risk asset volatility coupled with moderate returns. Stocks and bonds remain range bound while commodities appear to be breaking out from a long slump. Real rates remain negative across the developed markets, suggesting one should not get too negative.

We continue to recommend overweighting global equities with the focus on the non-US developed markets of Japan and Europe. Within Europe we remain focused on the Southern Tier markets, which are less exposed to tariff risk and have been the star performers year to date ( GO SOUTH January 2018). Likewise in Asia we remain focused on Japan, the ASEAN markets as well as China, which has sold off aggressively as tariff risk is priced in. Recent reserve rate reductions in China suggest better liquidity, which should support stock prices as should the impending A share inclusion into the MSCI EM index. The Asian equity markets have been laggards recently suggesting a catch up opportunity.

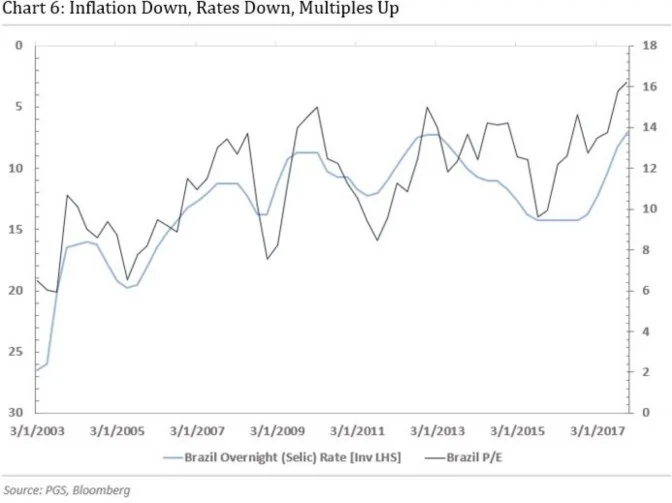

Within the Americas the focus remains south of the border. Brazil, which has also sold off on political and trade related concerns, seems quite interesting as its economic recovery continues, inflation stabilizes, interest rates decline and earnings and multiples expand. An election looms this fall but Brazil has been enduring political risk for the past several years suggesting it is priced in.

On a global sector basis we continue to recommend underweighting Tech and overweighting Financials, Industrials and Energy given strong earnings growth in the case of Energy and a global cap ex cycle in the case of Industrials. Energy stocks, particularly the oil majors, have lagged the crude rally which is supported by sharply declining inventory levels and rising geo political risk – a combination that would seem ripe for rising crude & stock prices. Small caps remain favored in all regions as a way to protect against currency movements and trade issues while also providing exposure to the production side of the global economy.

We continue to suggest an underweight position in Fixed Income driven by concerns over rising US Treasury supply coupled with reduced offshore demand. Rising currency hedging costs now eat up almost all the yield pickup UST offer foreign buyers. Expanding supply and a shrinking pool of buyers does not bode well for bond prices though its worth noting that only the US (among OECD nations) is forecast to increase its net debt to GDP ratio over the coming five years. It will be interesting to see if equities take rising long bond yields as growth positive. A steeper yield curve would be welcomed by banks (and the Fed).

Depressed yield levels & FX volatility mean that international sovereign debt is really a play on a weak dollar which bulging US twin deficits would seem to confirm. Given how low non-US sovereign yields are the currency tail is really wagging the fixed income dog. We continue to like US HY (favorable supply – demand, especially vs. IG) and preferred securities within the credit space.

In the Alternative segment we continue to recommend overweighting the Commodity sector given its late cycle characteristics together with depressed sentiment and lack of investor positioning, especially outside the oil space. We continue to favor the oil majors for their earnings and dividend/buyback capacity coupled with gold for the protection it offers against the uncertainties noted above.